FINANCIAL SERVICES EXPERIENCE MANAGEMENT

Re-imagine the financial services experience to build lasting, profitable relationships

In a highly regulated market, where margins are tight and product differentiation limited, experience is everything. For the world’s most iconic financial services companies, success is about more than just what they do — it’s about how they do it.

91 of the top 100 financial institutions rely on Qualtrics

They’re creating exceptional customer, product, brand, and employee experiences that help grow their brands and increase customer loyalty and lifetime value.

Join them on the world’s first Experience Management Platform™ and use real-time data, insights, and AI-powered recommendations to improve every moment that matters.

We work with the world’s leading banks, credit unions, insurance companies, brokers, financial advisors, and many more to help them deliver exceptional experiences.

Every journey, every channel. Optimised to drive loyalty and lifetime value

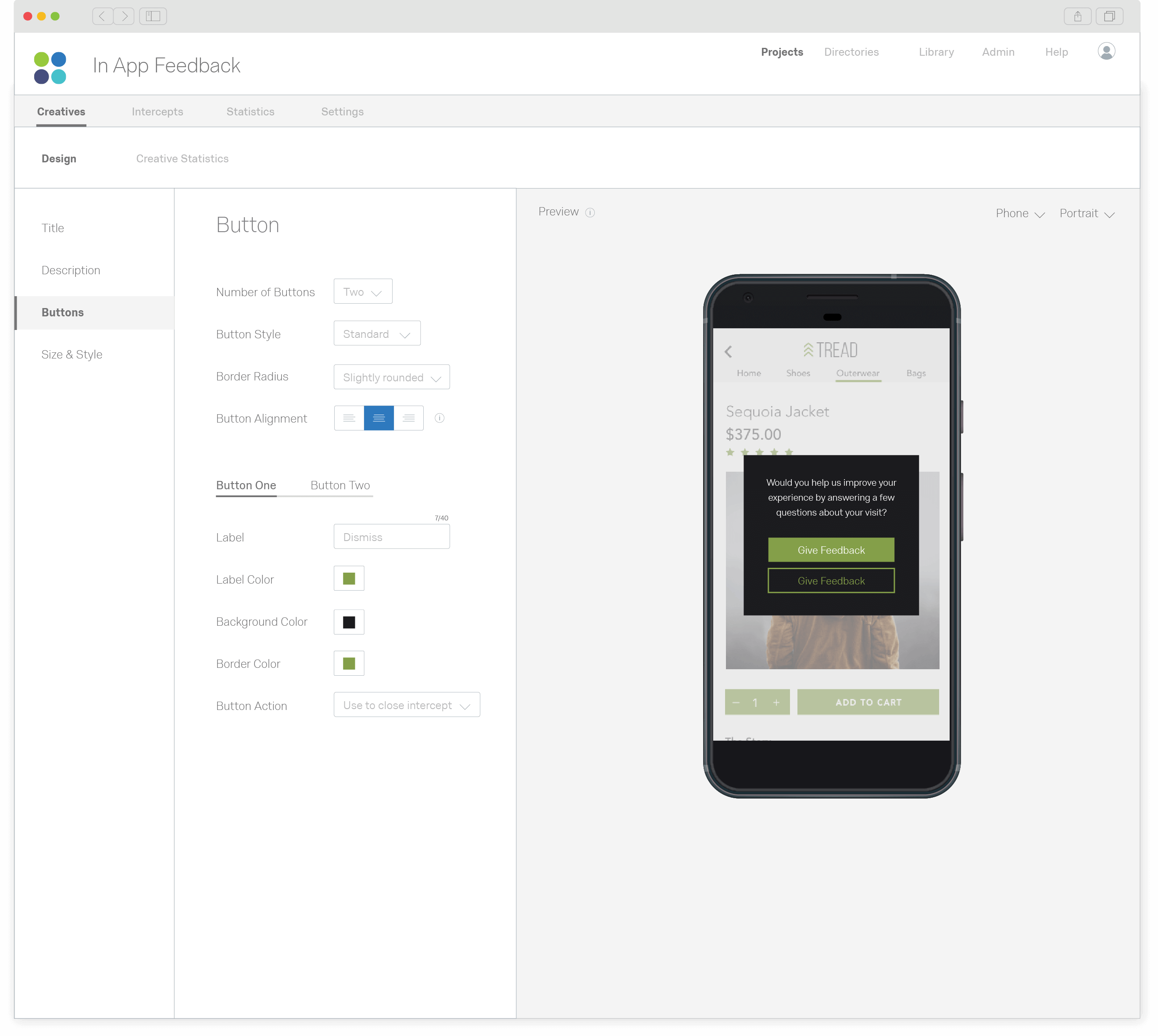

From customer onboarding to upselling, account management, and complaint resolution, make every interaction an opportunity to strengthen your customer relationships. Listen to customers, wherever they interact with you, spot experience gaps and take action automatically to improve the experience. With purpose-built products for every journey and channel, we’ll help you increase customer satisfaction and improve loyalty, acquisition, and customer lifetime value.

4 benefits of CustomerXM

- Identify experience gaps on every channel including websites, apps, in-branch, and contact center

- Understand the key drivers of satisfaction, loyalty, and spend

- Take action automatically to close experience gaps and resolve customer issues

- Coach frontline staff based on customer feedback with automatic recommendations and focus areas for improvement

Stop analysing. Start improving

Go straight to insights and improvements with iQ, our predictive intelligence engine that uses artificial intelligence to do the number crunching for you—automatically.

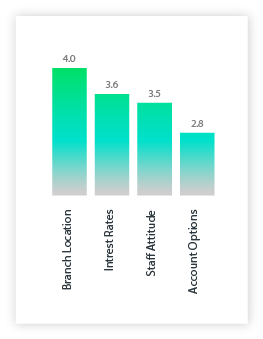

See what’s impacting your key metrics

Drive adoption and improve satisfaction rates across your digital channels with real-time experience data that helps you understand the why behind your most important metrics.

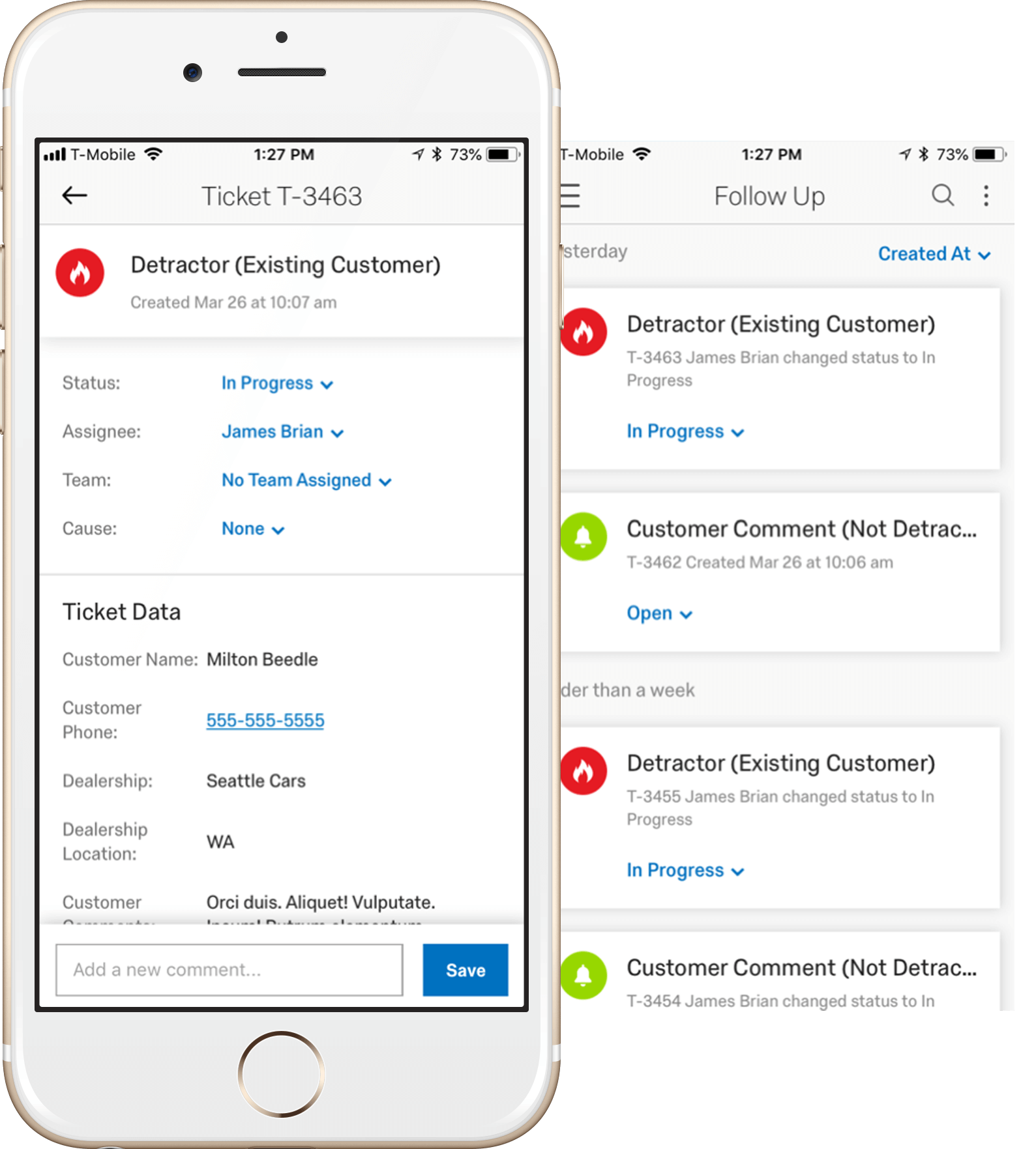

Take action at every level

From frontline branch teams and contact center agents to HQ staff, everyone in the organisation can see the actions they need to take to improve the experience for your customers.

Learn more about CustomerXM™

Learn MorePre-built financial services programs

Attract, engage, develop, and retain the industry’s best talent

Give everyone in the organisation the power to improve the experience for their teams. Hear every voice in the organisation and automatically recommend actions at every level to improve the experience. Managers will have the insights they need to drive improvements and develop their people, helping to improve engagement and deliver a better experience for customers too.

4 benefits of EmployeeXM

- Understand the key drivers of engagement, productivity, and more

- Optimise your recruiting, onboarding, training, and exit programs

- Enable managers throughout the organisation to improve the experience for their teams

- Understand the ROI of your HR initiatives and see their impact on key operational KPIs

Create a digital open door

Whatever the size of your organisation, listen to every employee with a digital open door that automates feedback, gathers it at scale, and understands your organisation’s hierarchy so the right people get the right information.

Get your people behind your biggest priorities

Whether it’s diversity and inclusion or refocusing your organisation on your customers, you’ll be able to track your progress and take actions that create a winning culture.

World-class stats. No degree required

Uncover insights hidden deep in your data with iQ—our predictive intelligence engine that does all the hard work and complicated calculations for you.

Learn more about EmployeeXM™

Learn MoreExpert-designed employee experience solutions

Products and packages tailored to your customers

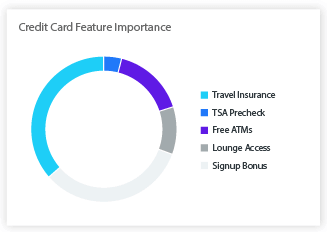

Understand what drives product satisfaction and spot opportunities for new packages and offers that will resonate with your target audience. You’ll be able to see which features customers love, how much they’re willing to pay, and what makes you stand out in a competitive market.

4 benefits of ProductXM

- Understand the key drivers of product success and spot gaps in the market for new products and services

- Launch new services and packages with complete confidence

- See at-a-glance how changes to your products will impact the bottom line

- Know the services customers are willing to pay for and how much they’re willing to pay

Perfect product packages. Straight out of the box

Identify perfect pairings of products, services and rewards to maximise cross-selling with our intuitive product optimiser tools. You’ll see how potential changes to your product set impact everything from sales to customer loyalty, giving you the confidence to launch new products and services that customers will love.

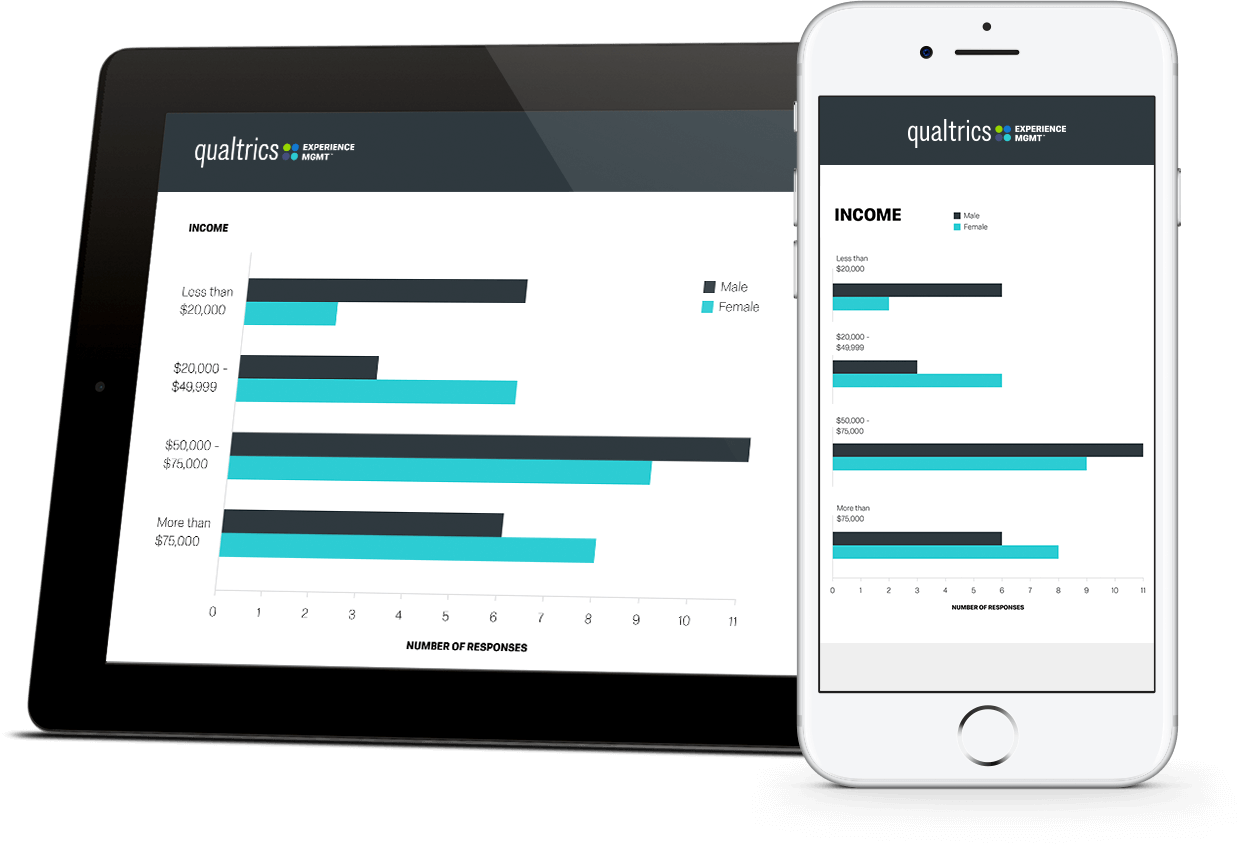

Understand your market inside out

Get a complete view of your potential customers with expert-designed market segmentation studies. You’ll see what matters most to different target customers and see at a glance the best opportunities for growth.

Digital products and services designed around customers

Win the battle for digital supremacy with customer feedback and user testing at the heart of your digital products. You’ll see what matters most to customers, what’s working well and the improvements that will have the biggest uptake on everything from satisfaction to frequency of use.

Learn more about ProductXM™

Learn MoreExpert-designed product experience solutions

Build trust and strengthen your brand

Monitor the health of your brand in real-time with comprehensive brand tracking, ad testing, and customer segmentation. Get a real-time view of your place in the market so that you can be the disruptor, not the disrupted.

4 benefits of BrandXM

- Launch new ad campaigns confidently with ad testing

- Keep all your stakeholders informed of your brand metrics with real-time data and automatic reporting

- Get up and running quickly with pre-built templates designed by financial services experts

- Understand how your brand is perceived on different channels and see what you need to do to improve them

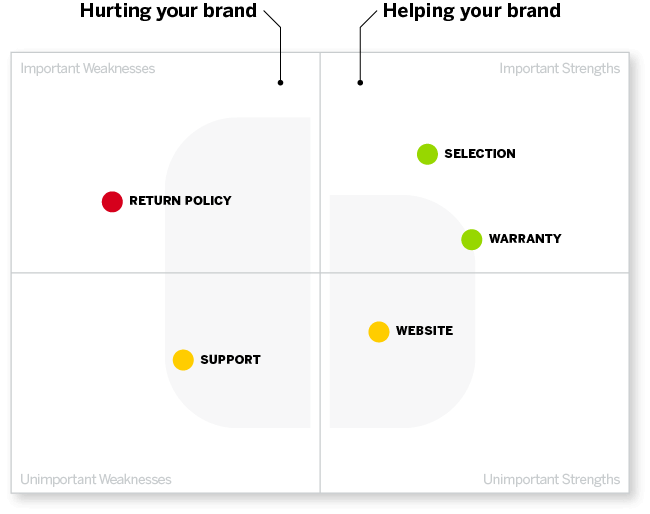

Prioritise your marketing spend

Driver iQ uses built-in analysis to help you focus your investments on the areas that will have the biggest impact on your growth.

Expertise at the click of a button

Whether it’s an ad testing survey, a brand tracker, or a segmentation study, access a library of pre-built projects and launch world-class brand experience programs with no expertise or prior experience.

Connect everything

Bring your operational data in from platforms like Salesforce, Marketo, and many more. With open APIs into operational data systems you’ll be able to see the impact of your brand strategy on the organisation’s core KPIs.